Palantir (PLTR 3.65%) has gained a reputation for being one of the best artificial intelligence (AI) investments, with its stock rising a whopping 320% since the start of 2024. However, looking at its current valuation, one could argue the expectations baked into its price may not necessarily be grounded in the company’s fundamentals.

Right now, Palantir is worth roughly $160 billion. However, I think there are a couple of AI stocks that could surpass Palantir in value by 2030. Those two candidates are Snowflake (SNOW 1.88%) and CrowdStrike (CRWD -1.76%).

Why these two? It all has to do with valuation.

Palantir has the least revenue growth of the three

Palantir and its AI software, which gives clients the tools they need to help with decision making, has become very popular in the AI space. However, Palantir’s growth hasn’t been remarkable. In the third quarter, Palantir’s revenue rose 30% year over year. While that’s strong, it’s nearly identical to what Snowflake and CrowdStrike latest quarterly revenue growth has been, at 28% and 29%, respectively.

Snowflake’s revenue growth was powered by its data cloud software platform that is necessary to store and provide data to AI models. On the other hand, CrowdStrike is a cybersecurity provider that uses AI to help determine what a threat is and what is normal activity. Obviously, from just the latest quarterly results, a true winner can’t be established.

However, over the last three years, Palantir’s cumulative revenue grew just 61%, while Snowflake and CrowdStrike grew revenues by 180% and 158%, respectively.

PLTR Revenue (Quarterly) data by YCharts.

Snowflake and CrowdStrike clearly have the edge over Palantir in topline growth, and it wouldn’t be surprising if Palantir struggles to justifying its current valuation. As anticipated, the three companies are valued at wildly different levels.

The market has given Palantir a massive premium over its peers, trading for an unbelievable 61 times trailing 12-month sales at the time of writing, which is why Palantir’s market cap is so much larger than its peers. But that price tag doesn’t seem normal, given Palantir’s growth level — even after accounting for its profitability (more on that later).

PLTR Market Cap data by YCharts.

This should be an obvious red flag for Palantir investors, as it’s unlikely to be able to maintain that valuation if its growth doesn’t accelerate. Still, there are some key reasons why Palantir is better off than CrowdStrike or Snowflake.

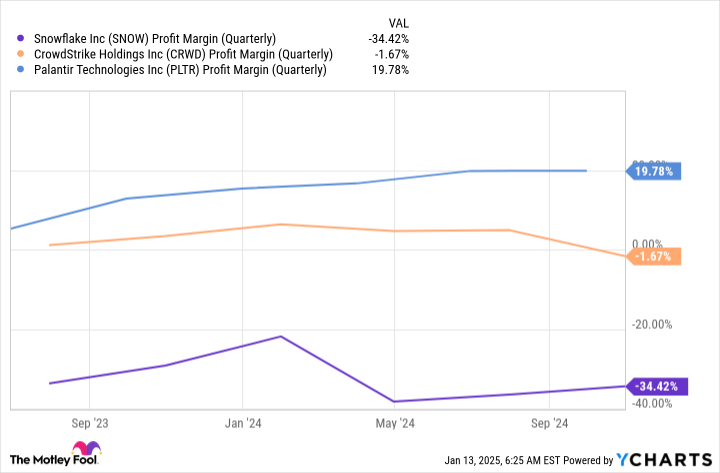

Palantir is the only solidly profitable company of this trio

One key advantage Palantir has over the other two is its profitability. Palantir is solidly profitable and has been so for some time. Snowflake and CrowdStrike haven’t been near the profitability levels Palantir has.

SNOW Profit Margin (Quarterly) data by YCharts.

This certainly gives Palantir an edge, and it accounts for some of the expensive price tag on its stock. After years of being deeply unprofitable (Snowflake) or teetering between the breakeven mark (CrowdStrike), the market may have some skepticism about whether these two can ever get over the hump and produce a solid profit margin like Palantir has. And sometimes the market can change its perception about stocks quickly, catching investors off guard.

Having said that, Palantir has set a great example for both companies to follow. In Q2 2022, Palantir’s loss margin was a dismal 38%. However, two quarters later, in Q4 2022, Palantir broke even and has steadily improved its profitability since. If either Snowflake or CrowdStrike have a Palantir moment and deliver strong profits, I wouldn’t be surprised to see these two outperform Palantir over the next five years. Because over this period, there’s a solid chance both companies will turn profitable.

Additionally, there’s the matter of Palantir’s very expensive stock. At the time of this writing, Palantir trades for staggering 359 times trailing earnings. Over the next five years, if Palantir maintains its 30% revenue growth rate and its 20% profit margin, that would value Palantir at 83 times trailing earnings if the stock stays at the same price it is right now.

On the other hand, what would happen if Snowflake and CrowdStrike could flip the switch and were profitable like Palantir? At today’s stock prices and revenue, if Snowflake and CrowdStrike were currently profitable mirroring Palantir’s 20% profit margin, the two would’ve been trading for only 83 times and 118 times trailing earnings, respectively, right now.

While, no doubt, both companies still have a ways to go before reaching Palantir’s profit levels, it also shows that they are far cheaper stocks than Palantir is, and with five years’ worth of growth ahead of them, it’s highly likely they’ll catch up in value with Palantir.

By 2030, I think that Snowflake and CrowdStrike will be worth far more than Palantir. This should likely occur through a combination of CrowdStrike and Snowflake achieving profitability, and Palantir’s valuation falling to a reasonable level.

Regardless, if you think Snowflake and CrowdStrike can achieve profitability over the next five years (like I do), they appear as a far better option to buy right now than Palantir.